Oct 13, 2025 • by Collins Nweke • Source: Collins Nweke •  373 views

373 views

- FCMB/NGN = ₦ 10.45

- FIDELITYBK/NGN = ₦ 20.15 FIDSON/NGN = ₦ 41.90

- FIRSTHOLDCO/NGN = ₦ 31.25 FTNCOCOA/NGN = ₦ 6.00

- GEREGU/NGN = ₦ 1,141.50 GTCO/NGN = ₦ 93.40

- GUINEAINS/NGN = ₦ 1.46 GUINNESS/NGN = ₦ 183.75

- HMCALL/NGN = ₦ 4.38 HONYFLOUR/NGN = ₦ 22.15

- IKEJAHOTEL/NGN = ₦ 19.95 IMG/NGN = ₦ 32.40

- INFINITY/NGN = ₦ 7.00 INTBREW/NGN = ₦ 14.75

- INTENEGINS/NGN = ₦ 2.98 JAIZBANK/NGN = ₦ 4.32

- JAPAULGOLD/NGN = ₦ 2.54 JBERGER/NGN = ₦ 134.00

- JOHNHOLT/NGN = ₦ 7.20 JULI/NGN = ₦ 8.95

- LASACO/NGN = ₦ 2.98 LEARNAFRCA/NGN = ₦ 6.55

- LEGENDINT/NGN = ₦ 5.80 LINKASSURE/NGN = ₦ 2.00

- LIVESTOCK/NGN = ₦ 7.50 LIVINGTRUST/NGN = ₦ 5.00

- MANSARD/NGN = ₦ 17.00 MAYBAKER/NGN = ₦ 17.05

- MBENEFIT/NGN = ₦ 3.85 MCNICHOLS/NGN = ₦ 3.22

- MECURE/NGN = ₦ 28.40 MEYER/NGN = ₦ 15.10

- MTNN/NGN = ₦ 471.00 MULTIVERSE/NGN = ₦ 13.90

- NAHCO/NGN = ₦ 113.00 NASCON/NGN = ₦ 100.00

- NB/NGN = ₦ 76.60 NCR/NGN = ₦ 16.00

- NEIMETH/NGN = ₦ 6.00 NEM/NGN = ₦ 29.15

- NESTLE/NGN = ₦ 1,893.00 NGXGROUP/NGN = ₦ 58.95

- NIDF/NGN = ₦ 113.00 NNFM/NGN = ₦ 93.65

- NPFMCRFBK/NGN = ₦ 2.99 NSLTECH/NGN = ₦ 0.85

- OANDO/NGN = ₦ 44.65 OKOMUOIL/NGN = ₦ 1,020.00

- OMATEK/NGN = ₦ 1.50 PRESCO/NGN = ₦ 1,479.90

- PRESTIGE/NGN = ₦ 1.69 PZ/NGN = ₦ 38.60

- REDSTAREX/NGN = ₦ 11.00 REGALINS/NGN = ₦ 1.43

- ROYALEX/NGN = ₦ 2.33 RTBRISCOE/NGN = ₦ 3.40

- SCOA/NGN = ₦ 6.59 SEPLAT/NGN = ₦ 5,917.20

- SKYAVN/NGN = ₦ 90.05 SOVRENINS/NGN = ₦ 3.47

- STANBIC/NGN = ₦ 116.85 STERLINGNG/NGN = ₦ 7.70

- SUNUASSUR/NGN = ₦ 5.77 TANTALIZER/NGN = ₦ 2.33

- THOMASWY/NGN = ₦ 3.01 TIP/NGN = ₦ 13.31

- TOTAL/NGN = ₦ 640.00 TRANSCOHOT/NGN = ₦ 164.60

- TRANSCORP/NGN = ₦ 48.50 TRANSEXPR/NGN = ₦ 2.15

- TRANSPOWER/NGN = ₦ 342.00 TRIPPLEG/NGN = ₦ 4.91

- UACN/NGN = ₦ 68.00 UBA/NGN = ₦ 42.40

- UCAP/NGN = ₦ 18.60 UHOMREIT/NGN = ₦ 51.85

- UNILEVER/NGN = ₦ 74.00 UNIONDICON/NGN = ₦ 8.00

- UNIVINSURE/NGN = ₦ 1.11 UPDC/NGN = ₦ 6.50

- UPDCREIT/NGN = ₦ 7.30 UPL/NGN = ₦ 5.50

- VERITASKAP/NGN = ₦ 2.16 VFDGROUP/NGN = ₦ 10.80

- VITAFOAM/NGN = ₦ 84.50 WAPCO/NGN = ₦ 130.00

- WAPIC/NGN = ₦ 3.30 WEMABANK/NGN = ₦ 18.40

- ZENITHBANK/NGN = ₦ 68.10

- ABBEYBDS/NGN = ₦ 6.80 ABCTRANS/NGN = ₦ 4.05

- ACADEMY/NGN = ₦ 9.60 ACCESSCORP/NGN = ₦ 25.75

- AFRIPRUD/NGN = ₦ 15.00 AIICO/NGN = ₦ 3.97

- AIRTELAFRI/NGN = ₦ 2,310.50 ARADEL/NGN = ₦ 628.00

- AUSTINLAZ/NGN = ₦ 2.90 BERGER/NGN = ₦ 36.55

- BETAGLAS/NGN = ₦ 486.00 BUACEMENT/NGN = ₦ 160.00

- BUAFOODS/NGN = ₦ 629.70 CADBURY/NGN = ₦ 69.00

- CAP/NGN = ₦ 70.00 CAVERTON/NGN = ₦ 6.67

- CHAMPION/NGN = ₦ 16.00 CHAMS/NGN = ₦ 4.10

- CHELLARAM/NGN = ₦ 16.25 CILEASING/NGN = ₦ 6.05

- CONOIL/NGN = ₦ 211.10 CORNERST/NGN = ₦ 6.20

- CUSTODIAN/NGN = ₦ 44.00 CUTIX/NGN = ₦ 3.67

- CWG/NGN = ₦ 18.15 DAARCOMM/NGN = ₦ 1.10

- DANGCEM/NGN = ₦ 585.60 DANGSUGAR/NGN = ₦ 59.70

- DEAPCAP/NGN = ₦ 1.71 ELLAHLAKES/NGN = ₦ 13.30

- ENAMELWA/NGN = ₦ 42.45 ETERNA/NGN = ₦ 41.00

- ETI/NGN = ₦ 35.30 ETRANZACT/NGN = ₦ 15.00

- EUNISELL/NGN = ₦ 44.00 FCMB/NGN = ₦ 10.45

- FIDELITYBK/NGN = ₦ 20.15 FIDSON/NGN = ₦ 41.90

- FIRSTHOLDCO/NGN = ₦ 31.25 FTNCOCOA/NGN = ₦ 6.00

- GEREGU/NGN = ₦ 1,141.50 GTCO/NGN = ₦ 93.40

- GUINEAINS/NGN = ₦ 1.46 GUINNESS/NGN = ₦ 183.75

- HMCALL/NGN = ₦ 4.38 HONYFLOUR/NGN = ₦ 22.15

- IKEJAHOTEL/NGN = ₦ 19.95 IMG/NGN = ₦ 32.40

- INFINITY/NGN = ₦ 7.00 INTBREW/NGN = ₦ 14.75

- INTENEGINS/NGN = ₦ 2.98 JAIZBANK/NGN = ₦ 4.32

- JAPAULGOLD/NGN = ₦ 2.54 JBERGER/NGN = ₦ 134.00

- JOHNHOLT/NGN = ₦ 7.20 JULI/NGN = ₦ 8.95

- LASACO/NGN = ₦ 2.98 LEARNAFRCA/NGN = ₦ 6.55

- LEGENDINT/NGN = ₦ 5.80 LINKASSURE/NGN = ₦ 2.00

- LIVESTOCK/NGN = ₦ 7.50 LIVINGTRUST/NGN = ₦ 5.00

- MANSARD/NGN = ₦ 17.00 MAYBAKER/NGN = ₦ 17.05

- MBENEFIT/NGN = ₦ 3.85 MCNICHOLS/NGN = ₦ 3.22

- MECURE/NGN = ₦ 28.40 MEYER/NGN = ₦ 15.10

- MTNN/NGN = ₦ 471.00 MULTIVERSE/NGN = ₦ 13.90

- NAHCO/NGN = ₦ 113.00 NASCON/NGN = ₦ 100.00

- NB/NGN = ₦ 76.60 NCR/NGN = ₦ 16.00

- NEIMETH/NGN = ₦ 6.00 NEM/NGN = ₦ 29.15

- NESTLE/NGN = ₦ 1,893.00 NGXGROUP/NGN = ₦ 58.95

- NIDF/NGN = ₦ 113.00 NNFM/NGN = ₦ 93.65

- NPFMCRFBK/NGN = ₦ 2.99 NSLTECH/NGN = ₦ 0.85

- OANDO/NGN = ₦ 44.65 OKOMUOIL/NGN = ₦ 1,020.00

- OMATEK/NGN = ₦ 1.50 PRESCO/NGN = ₦ 1,479.90

- PRESTIGE/NGN = ₦ 1.69 PZ/NGN = ₦ 38.60

- REDSTAREX/NGN = ₦ 11.00 REGALINS/NGN = ₦ 1.43

- ROYALEX/NGN = ₦ 2.33 RTBRISCOE/NGN = ₦ 3.40

- SCOA/NGN = ₦ 6.59 SEPLAT/NGN = ₦ 5,917.20

- SKYAVN/NGN = ₦ 90.05 SOVRENINS/NGN = ₦ 3.47

- STANBIC/NGN = ₦ 116.85 STERLINGNG/NGN = ₦ 7.70

- SUNUASSUR/NGN = ₦ 5.77 TANTALIZER/NGN = ₦ 2.33

- THOMASWY/NGN = ₦ 3.01 TIP/NGN = ₦ 13.31

- TOTAL/NGN = ₦ 640.00 TRANSCOHOT/NGN = ₦ 164.60

- TRANSCORP/NGN = ₦ 48.50 TRANSEXPR/NGN = ₦ 2.15

- TRANSPOWER/NGN = ₦ 342.00 TRIPPLEG/NGN = ₦ 4.91

- UACN/NGN = ₦ 68.00 UBA/NGN = ₦ 42.40

- UCAP/NGN = ₦ 18.60 UHOMREIT/NGN = ₦ 51.85

- UNILEVER/NGN = ₦ 74.00 UNIONDICON/NGN = ₦ 8.00

- UNIVINSURE/NGN = ₦ 1.11 UPDC/NGN = ₦ 6.50

- UPDCREIT/NGN = ₦ 7.30 UPL/NGN = ₦ 5.50

- VERITASKAP/NGN = ₦ 2.16 VFDGROUP/NGN = ₦ 10.80

- VITAFOAM/NGN = ₦ 84.50 WAPCO/NGN = ₦ 130.00

- WAPIC/NGN = ₦ 3.30 WEMABANK/NGN = ₦ 18.40

- ZENITHBANK/NGN = ₦ 68.10

LATEST UPDATES

Founder of Zenith Bank, Jim Ovia Reaffirms Strong Commitment to Shareholder Value at the NGX Closing Gong Ceremony

2 hours ago Share

Nigeria’s Crude Oil Production Falls to 1.39mb/d in September 2025

5 hours ago Share

Business | Business Regulations, Law & Practice

Trademark Enforcement in Nigeria: Commentary on the Decision of the Federal High Court – Elo Othuke Azaino v. Sterling Bank Plc

8 hours ago Share

Nigeria in 1min: Economic, Business and Financial Headlines – 151025

14 hours ago Share

Nigeria Secures Another $2bn Gas Investment from Shell

Tuesday, 14th at 6:46 PM Share

Oil Market Braces for Contango and Shale Slowdown – OIR 141025

Tuesday, 14th at 6:14 PM Share

Equities Market Halts Bullish Run as Investors Lost N3.98bn on Tuesday; BDC Rate Appreciates to N1,485/US$1

Tuesday, 14th at 5:38 PM Share

FCCPC, CBN Strengthen Collaboration to Enforce 48-Hour Deadline for Transaction Reversals

Tuesday, 14th at 12:40 PM Share

Nigeria’s Domestic Debt Rises 2% Q-o-Q to N76.6trn in Q2 2025

Tuesday, 14th at 11:17 AM Share

Market | Stock & Analyst Updates

Zenith Bank Signals Strong Full-Year Outlook with N51.3bn Interim Dividend Payout

Tuesday, 14th at 8:59 AM Share

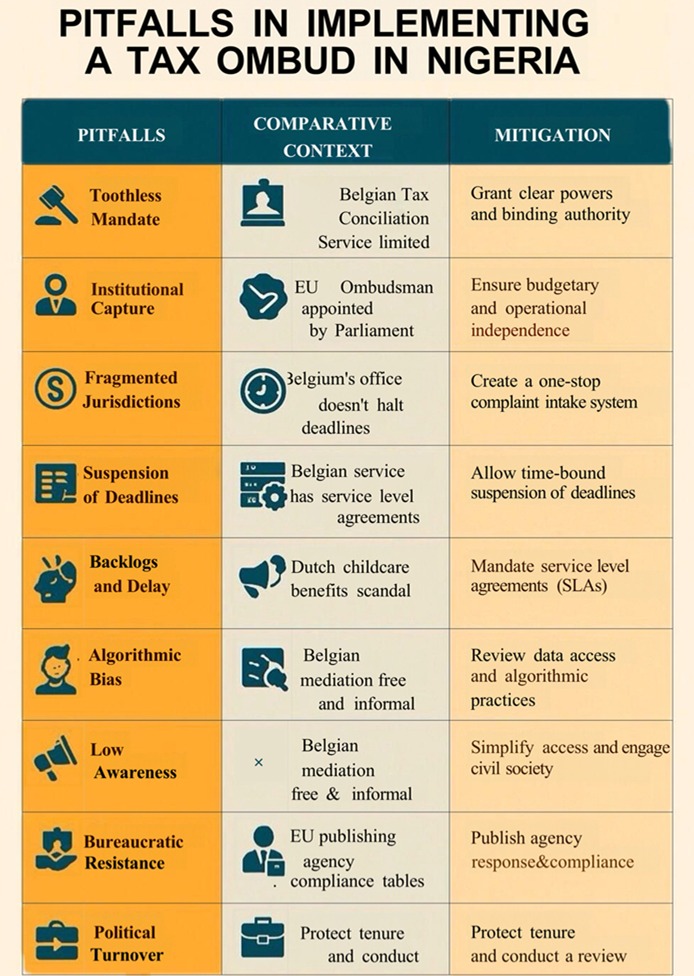

When the Federal Government of Nigeria announced its intention to establish a Tax Ombudsman, it marked an important step toward humanising Nigeria’s tax system. For too long, taxpayers have faced an impersonal, often intimidating bureaucracy that viewed them primarily as revenue sources rather than stakeholders in a social contract. The proposed Ombud, if well designed, could change that. The reason is simple. It should provide redress, transparency, and fairness in tax administration.

But there is a caveat. In governance reform, the road from intention to impact is treacherous. Nigeria’s political economy is littered with good ideas that are often buried under poor implementation. The Tax Ombud will be no exception unless we learn from international models, especially those that blend independence, accessibility, and accountability. Drawing on decades of experience operating within the Belgian and EU tax jurisdictions, as well as research into other well-functioning tax regimes, I have attempted to envision the potential pitfalls ahead. There are equally proposed mitigations to consider.

The Trust Deficit Factor

The timing of this Tax Ombud proposal is strategic. Nigeria is seeking to widen its non-oil tax base amid fiscal constraints, while rebuilding trust in state institutions. Public acceptance of new taxes depends on perceived fairness. Citizens who distrust the process will not willingly comply. A credible Tax Ombud could thus be the missing link. It will serve as a bridge between enforcement and empathy.

In Belgium, for example, the ‘Fiscale bemiddelingsdienst’ (Tax Mediation Service) performs this exact bridge function. It enables individuals and companies to resolve disputes quickly, at no charge, and often informally. However, it is limited to mediation. It cannot overturn tax assessments or halt deadlines. The model demonstrates accessibility and efficiency but also reveals a crucial lesson: without limited binding authority, an Ombud risks becoming a mere complaint box. Nigeria must therefore go further. It should retain the accessibility of the Belgian model, but give the office teeth to bite where fairness demands it.

A Ten-Point Pitfall

Similarly, a good doctor prescribes medications based on an accurate diagnosis; the establishment of the Tax Ombud for Nigeria and the path leading to it is strewn with several pitfalls. As we will read in the analysis that follows, the Belgian Tax Ombudsman equally faced challenges. Citizens suffered unintended consequences. However, these challenges continue to be re-examined and adapted to the spirit of the time and a constantly evolving environment. From the outset, it is prudent to examine Nigeria’s plan, not by reinventing the wheel, but by drawing on examples elsewhere.

Source: https://www.collinsnweke.eu/

Pitfall 1: A Toothless Mandate

In Nigeria, a weak or ambiguous legal framework could cripple the Tax Ombud before it begins. If the Ombud’s decisions are only advisory, if it cannot compel a response from the tax authority, or if its jurisdiction overlaps confusingly with the Tax Appeal Tribunal (TAT), the system will collapse under its own contradictions.

Belgium’s experience is instructive. Its conciliation office is efficient precisely because it confines itself to mediation. That limitation works only in a well-ordered system where statutory rights are respected and trust in government is high. Nigeria’s context is the opposite: institutional distrust, delayed refunds, and opaque assessments are common. Nigerians will demand more than “soft power” remedies.

What Nigeria could do: The enabling law must define clear powers and timelines. The Ombud should be able to:

- require responses from tax authorities within fixed deadlines;

- issue limited binding recommendations in procedural matters (e.g., response delays, refund verification); and

- publish unresolved cases with agency explanations; naming and shaming, if necessary.

Transparency, not just authority, is the true currency of legitimacy.

Pitfall 2: Institutional Capture and Budgetary Dependence

No Ombud can be effective if the same agencies control its purse strings it must oversee. Nigeria’s history with regulatory bodies shows that budget manipulation is a favourite weapon of capture.

The EU Ombudsman offers a contrasting picture. Appointed through a parliamentary process, it enjoys operational autonomy and a fixed budget under the European Parliament, not the executive. Similarly, Canada’s Taxpayers’ Ombudsperson reports directly to the Minister of National Revenue but is guided by a codified Taxpayer Bill of Rights. This is a charter that protects both taxpayers and the Ombud itself from political interference.

Nigeria’s fix: Guarantee financial and administrative independence through:

- a ring-fenced budget approved by the National Assembly, not the tax agency;

- fixed tenure for the Ombud, removable only for cause; and

- quarterly public reports to the National Assembly and citizens.

If political actors cannot starve it, they cannot silence it. This should be the mindset shielding the Tax Ombud from institutional capture.

Pitfall 3: Fragmented Jurisdictions

Nigeria’s tax ecosystem is famously chaotic. Federal, state, and local authorities all levy overlapping taxes. A small business may deal with three different tax offices in one fiscal year. An Ombud that handles only federal complaints would therefore miss the heart of taxpayer frustration.

Belgium faced a similar problem. Its federal Tax Mediation Service cannot mediate disputes relating to regional or municipal taxes. The resulting fragmentation leaves taxpayers confused about where to turn. Nigeria must not replicate that structural error.

Mitigation:

- Establish Memoranda of Understanding (MoUs) with state revenue boards and local councils.

- Create a “one-stop complaint intake”—citizens file once, and the Ombud routes the case to the right tier of government.

- Publish an annual “competence map” showing which body handles which tax matters.

Simplify access, and compliance will follow.

Pitfall 4: No Suspension of Deadlines

Under the Belgian model, lodging a complaint does not pause legal deadlines for filing appeals or paying taxes. That design makes sense in a system where taxpayers and the state act in good faith. In Nigeria, where administrative delays are endemic, such rigidity would make the Ombud’s relief meaningless.

Mitigation:

Give the Ombud a narrow, time-bound suspension power. For example, a 30-day standstill where a taxpayer shows prima facie hardship or error. This will protect citizens without undermining fiscal discipline.

Pitfall 5: Backlogs and Bureaucratic Delay

In public administration, justice delayed is justice denied. A slow Ombud will fail even if its decisions are sound.

Belgium’s service acknowledges receipt of complaints within five working days and decides on admissibility within fifteen. Canada’s office contacts complainants within five business days 95% of the time. These Service Level Agreements (SLAs) build public trust.

Nigeria’s remedy: Legally mandate SLAs for every process stage; acknowledgement, admissibility, investigation, resolution; and publish real-time dashboards showing performance. Citizens should not need to guess where their complaint stands.

Pitfall 6: Weak Data Systems and Poor Interoperability

Effective investigation requires access to tax records, correspondence logs, and payment histories. Nigeria’s tax data remains siloed between the Federal Inland Revenue Service (FIRS), state boards, and identity registries (NIN/BVN). Without integration, the Ombud will be blind.

Mitigation:

- Provide statutory rights of data access for the Ombud.

- Build a case management platform interoperable with FIRS and state systems.

- Publish quarterly reports on data-access bottlenecks and agency compliance.

Data transparency is not a luxury; it is the oxygen of modern oversight.

Pitfall 7: Algorithmic Bias and Systemic Injustice

An emerging frontier in tax administration is algorithmic risk profiling. This is the use of automated systems to flag taxpayers for audit. While efficient, such systems can encode bias. The Dutch childcare benefits scandal is a sobering case in point that offers a meek lesson. Thousands of innocent families were wrongly accused of fraud due to biased algorithms.

Nigeria’s safeguard: The Ombud should have explicit jurisdiction to review systemic or algorithmic practices. It should be empowered to recommend the suspension of any automated enforcement that produces discriminatory outcomes.

Periodic Algorithmic Impact Assessments must be mandated for all tax technologies.

Pitfall 8: Low Awareness and Elite Capture

An Ombud unused by ordinary citizens is no Ombud at all. There is a real risk that only large corporations and well-connected taxpayers will exploit the service, leaving MSMEs and informal workers excluded.

Belgium’s practice is a helpful contrast: mediation is open, free, and informal. Citizens can complain via phone, email, or post. The process is simple, not intimidating.

Nigeria’s adaptation:

- Provide multilingual complaint channels (including Pidgin and major local languages).

- Open regional desks and mobile “ombud clinics” for MSMEs.

- Partner with civil society, accountants, chambers of commerce, and (yes!) social media influencers for outreach.

Public trust grows through visibility, not only slogans.

Pitfall 9: Bureaucratic Resistance

Tax agencies are not famous for humility. They may stonewall, ignore Ombud queries, or downplay recommendations. The EU Ombudsman overcomes this by publishing compliance tables showing which agencies respond and how fast. Reputation becomes the enforcement tool.

Nigeria should adopt the same transparency. Every quarter, publish a “name and compliance” table of agencies, showing their response times and implementation rates. Public exposure will achieve what internal memos cannot.

Pitfall 10: Political Turnover and Reform Fatigue

Many Nigerian institutions start strong and fade after a change in administration. Continuity must be engineered, not assumed.

Mitigation:

- Enshrine the Ombud in law, not executive decree.

- Protect its leadership tenure.

- Require mandatory annual reviews by an independent panel drawn from the legal, business, and civil society sectors.

Institutional memory must outlive political memory.

Measuring Success With Key Performance Indicators (KPIs)

Three years after launch, Nigerians should be able to ask: has the Ombud changed anything? The answer must be measurable.

- Response and resolution time (benchmarked against Belgium and Canada).

- Share of cases from outside major cities.

- Rate of compliance with Ombud recommendations.

- Reduction in repeated complaints on the same issue.

- Annual taxpayer satisfaction index.

If these numbers move in the right direction, voluntary compliance will follow. And so will revenue.

Final Analysis: The Human Face of Tax Reform

Democratic taxation is not about extracting revenue. It should be about reciprocity and trust. When citizens feel heard, they are more likely to comply. When they feel cheated, they evade. The Tax Ombud could therefore become the human face of Nigeria’s fiscal reforms.

Belgium shows the virtue of accessibility. The EU shows the power of transparency. Canada shows the discipline of clear rights and timelines. Nigeria is well-positioned to combine all three: access, transparency, and enforceability. There is perhaps no other known way for the Tax Ombud of Nigeria to transcend good intentions than by embracing international best practices. Done right, this institution could redefine the relationship between taxpayers and government. Done wrong, it will be one more reform that began with applause and ended in deafening silence.

References & Further Reading

- PwC Nigeria, ‘The 2025 Fiscal Reforms: Consolidating the Tax Landscape,’ Policy Brief, June 2025.

- Belgian Federal Public Service Finance, ‘ Belastingbemiddelingsdienst – Wie zijn wij? (accessed 11 October 2025).

- Ibid.; see also FOD Finance, ‘Procedure en deadlines.’

- European Ombudsman, ‘Annual Report 2024.’

- Office of the Taxpayers’ Ombudsperson (Canada), ‘Service Standards,’ 2024.

- Dutch Parliamentary Inquiry Committee, ‘Childcare Benefits Scandal Report,’ 2021.

- European Parliament, ‘Statute of the European Ombudsman,’ Art. 8.

- Belgian FOD Finance, ‘Fiscale bemiddelingsdienst – jaarverslag 2023’

- Office of the Taxpayers’ Ombudsperson (Canada), op. cit.

- Dutch Parliamentary Inquiry Committee, op. cit.

- Belgian FPS Finance, ‘Belastingbemiddelingsdienst – Hoe dien ik een verzoek in?’

- European Ombudsman, ‘Case Digest 2023: Transparency and Compliance in EU Institutions.’

About the AUTHOR

This research was authored by Collins NWEKE, an International Trade Consultant & Economic Diplomacy researcher. He was a former Green Councillor at Ostend City Council, Belgium, where he served three consecutive terms until December 2024. He is a Patron of The AfrikaFora. Collins is a Fellow of both the Chartered Institute of Public Management of Nigeria and the Institute of Management Consultants. He is also a Distinguished Fellow of the International Association of Research Scholars & Administrators, serving on its Governing Council. A columnist for The Brussels Times, Proshare, and Global Affairs Analyst with a host of media houses, Collins writes from Brussels, Belgium. X: @collinsnweke E: admin@collinsnweke.eu W: www.collinsnweke.eu